Home » Posts tagged 'surprise medical bills'

Tag Archives: surprise medical bills

Monday at 1 PM: a webinar featuring Dr. Marty Makary, Leah Binder, and Marshall Allen

Dear TSW nation,

So maybe this posting is not funny like last month’s, when Angioscreen won the uncoveted Deplorables Award. But “funny” isn’t going to give you insights into how to perform more effectively — other than, of course, not using Angioscreen, a decision that will benefit your workforce immeasurably.

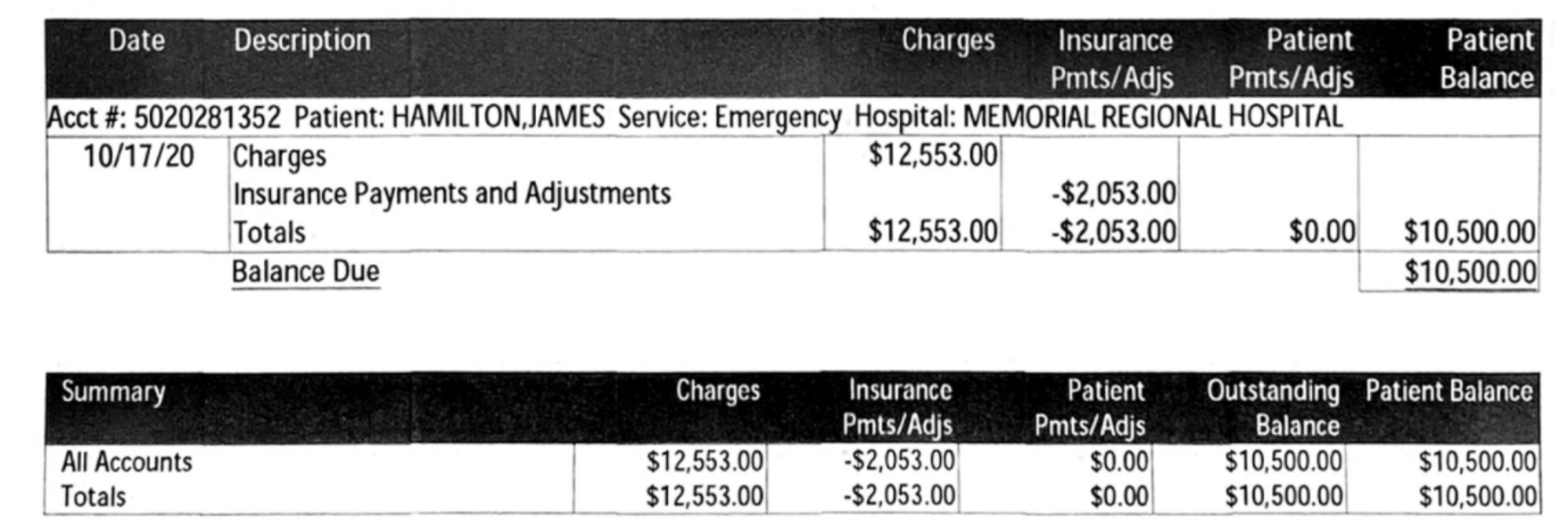

This posting has a bit more substance to it, announcing a webinar Monday, March 22nd at 1 PM EDT on “Hospital Financial Ethics.” It will feature a real price-gouging incident with a real bill — and a real patient with a real name (James Hamilton).

This bill will be deconstructed by an expert panel. I am humbled (which doesn’t happen often) by the talent we’ve been able to attract to this panel, none of whom even need an introduction:

- Marty Makary

- Leah Binder

- Marshall Allen

And as long as you are signing up for our webinars, there are more on the docket (all at 1 PM EDT)

April 7: An “Emergency Webinar” on overcoming vaccine hesitancy in your workforce.

April 22: The best premature birth avoidance technology we have ever seen…and we never endorse vendors. We’re making an exception here because they actually do something that employees love and saves money besides.

May 12: The Top Ten Easiest Employee Behavior Changes. Turns out — who knew? — that employees can’t keep weight off, they don’t like broccoli, and they already buckle their seat belts. But there are ten behavior changes that either save money or improve health or both, that are so easy to make you don’t need to bribe or fine them.

June 15: Never Pay the First Bill. A pre-publication look at Pro Publica uber-investigator Marshall Allen’s new book of the same name on how not to get snookered by a healthcare bill.

July 15: Featuring Dr. Eric Bricker (yes, the very same) on aligning incentives with your providers, your PBMs and your consultants.

Share this:

Surprise bills meet COVID: What you need to know

Ooooh….yikes. We just did a webinar on this very topic, with Dave Chase and Doug Aldeen. And you missed it. We know what it feels like to miss things.

So, there is a reprise, covering surprise medical bills and COVID, being offered next Thursday, at 2 PM EDT, by our friends at a wellness company called Wellable. Yes, I know it seems out-of-character for us to use the phrase “our friends at a wellness company,” but there are plenty of upstanding wellness companies that we are thrilled to be associated with, like US Preventive Medicine, with whom we may do a joint webinar this summer.

Indeed many stranger things have happened. Case in point: Ron Goetzel himself — the very same Ron Goetzel who we have blown the whistle on multiple times — once publicly gave Quizzify a shout-out as being “lots of fun and very clever.” That was before he tried walk it back, like in this Seinfeld episode.

So what’s going on here?

No, we haven’t all just entered this.

Nor have pods taken over our bodies. (Though I suspect, if pods had taken over our bodies, they wouldn’t admit it.)

Quite the opposite, we find common ground with almost any ethical, competent company in this field, of which Wellable is one.

We invite you to join their webinar and look forward to answering your questions.

Spoiler alert: we have figured out how to solve your surprise bill problem, for most non-elective situations, by combining Marty Makary’s “battlefield consent” with reference-based pricing. You can implement this solution very easily.

No need to take our word for this. Our solution was featured in the New York Times.

Seats are limited, so register as fast as you can…

Share this:

Surprise billing and COVID: The Ultimate Podcast

Before continuing with this posting, we would like to acknowledge the heroic efforts of frontline healthcare workers, risking their own health and even lives to save others. These are not the people sending the bills. That would be the private equity-controlled hospitals and specialty groups. it is important to draw a bright line between these cohorts.

You might have read somewhere that surprise bills are not allowed by hospitals taking funds under the CARES Act. This is true. The patient share is limited to what they would have paid in-network.

So who do you think is paying that bill? Look at the person six feet to your left. Now look at that person six feet to your right. All three of you are.

This bill isn’t a price control for out of network providers. The bills don’t automatically get lower. Only the patients are protected. This actually makes surprise-billing much easier, because the employee is not likely to complain if it’s not their bill. Who even reads the EOB? How many employees even know wht EOB stands for?

Recently DirectPath released a report called the Health Care Literacy Gap. In it, they noted that 55% of employees already don’t complain about billing errors, because they don’t feel it’s worth the effort.

Why don’t they feel it’s worth the effort? Let’s put it this way: when was the last time you didn’t complain about a billing mistake at a restaurant, hotel, etc. ?(Yes, we know it was more than a month ago. We are being figurative here.) That’s because it’s your money.

But if the waiter or hotel manager came over and, instead of presenting a bill, said the whole thing was on the house? Would you ask to review the bill and point out mistakes? And that’s exactly what could happen if patients are held harmless from out-of-network charges due to COVID.

COVID treatment should be free in any case. But if you read the CARES Act closely, it appears that even patients testing negative who are then treated for something else may be immune from surprise bills. Once again, who do you think is paying?

And you can bet there will be more of them than ever in 2020. That’s because the private equity companies are counting on the facts not just that employees won’t complain, but that your overall healthcare spend will be way down…and as a result you won’t carefully review your individual charges.

This of course doesn’t include the surprise bills employees will get as a result of other emergency visits, admissions, and deliveries. Heart attacks aren’t going away.

Fortunately, there is a solution. You can implement it posthaste. It’s all wrapped up in this podcast. The podcast features not only me, but uberbroker David Contorno, ERISA guru Doug Aldeen, and Rachel Miner, who in addition to being a successful broker, actually had the unfortunate chance to have to use our surprise bill “hack” in a North Carolina emergency room. North Carolina provider are notorious for their high-multiple-of-Medicare pricing, but this hack you’ll be hearing about kept her bill to a paltry 2x Medicare, including for any out-of-network “ologists” consulting on her son’s case.

Share this:

Corona-meets-surprise bills: six things you don’t wanna know

Thanks to corona, surprise bills are ba-ack. And as you read below, you’ll see why coronabills will be a thing in 2020.

You can listen to a new podcast on this exact topic when you go to work. That is, assuming, you either work in an essential industry that you need to actually go to, such as supermarkets, first-responding or healthcare (and thank you for that!!!), or you work at a place where you can easily socially distance, such as repairing Maytags, arguably the safest job on earth.

The private equity firms that own these out-of-network practices are no doubt relieved that surprise bills have magically disappeared from the headlines — but they have not magically disappeared from your claims spend. PE firms have not suddenly decided en masse to become good citizens. Quite the opposite – their other investments are foundering, with out-of-network providers being the bright spots in their portfolio. All thanks to surprise billing.

Here are three of the Six Things You Need to Know about Coronabills.

1. There is zero chance of federal surprise billing legislation this year

Consider the rather sketchy ad campaign run in “swing districts” last year by the private equity firms owning these practices. The theme was that if doctors don’t get paid enough, there won’t be enough doctors.

Well, as effective as that campaign apparently was in 2019 (you didn’t see any surprise bill prohibition passed into law, right?), imagine how effective it would be in 2020. All they would need is a few live shots of overwhelmed emergency rooms, which aren’t exactly hard to come by.

Prediction: it’s not just that nothing will pass. You won’t even see a bill make it out of Committee this year.

2. Because your total health spending will drop precipitously in 2020, you won’t carefully parse your bills

Executives pay more attention to healthcare spending – or any budget item – when it is rising. Elective procedures and doctor visits are so far off this year that total spend will decline. Hence you probably won’t even notice these surprise bills.

3. The canary in the coal mine would be employee complaints about surprise bills. Except that the copay is zero in many cases

As an ERISA plan, you don’t have to offer full coverage for treatment. But most of you will follow your carrier’s guidance. Which is to say, you will offer full coverage. Hence employees won’t be balance-billed. And that in turn means they won’t notice the total bill. Or, if they do notice, they won’t care. Bottom line: these bills won’t come to your attention.

Interested in more? Listen to the podcast or click through to Quizzify’s blog post on coronabills.

Share this:

New York Times features our solution to surprise bills!

Dear They Said What? Nation,

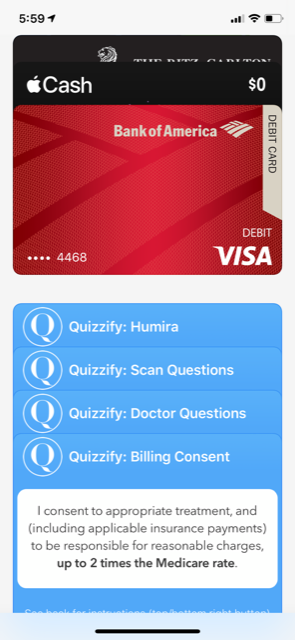

I think most of TSW Nation has already downloaded our custom consent to sign in emergency situations, in lieu of whatever they put in front of you. You can put this consent — along with some other helpful conversation-starters for other medical issues in doctor visits — right into your Apple Wallet. (Android users are out of luck until a future software update in which the Wallet App is added.)

Your Wallet should look like this (I mean, assuming you also bank at Bank of America)…

…and then tap where it says: “Billing Consent” to open this up:

If you haven’t already done so, well, today’s New York Times should be enough to convince you.

We’d encourage you to read the whole shebang but we’d be lying if we didn’t say this is our favorite part:

But, by writing in their own limits, patients might have leverage in negotiations or even in courts if out-of-network payment disputes arise, or at least proof they didn’t agree to pay the total charges, say some advocates and legal scholars.

Patients who try this could still get hit with a large balance bill. But “the difference is you can say ‘I offered this, but they refused it,’” rather than signing the original agreement to pay all charges, said Al Lewis, chief executive of Quizzify, an employee health care education company, who is a proponent of setting your own terms.

He came up with the twice-Medicare benchmark, even putting suggested wording for patients to print and carry with them on downloadable wallet cards, because he says it’s an amount that’s defensible.

If a hospital later turns down “two times Medicare and it goes to court, their lawyer is going to say, ‘We could lose this thing,’” said Mr. Lewis.

And, while I will be very pleased to take credit for inventing the consent in question (no “fake news” in this article!), I do want to give shout-outs to Marilyn Bartlett, David Contorno and Marty Makary. They provided the peanut butter (reference-based pricing) and chocolate (“battlefield consents”) and all I did was combine them.

And thank you to Stacey Richter for being the taste-tester. I was pretty sure this should work, but she was the one who proved it would work. In the immortal words attributed to the great philosopher Yogi Berra: “In theory, theory and practice are the same. In practice, they’re different.”

Not this time.

Share this:

Last call for Thursday’s “The cure for surprise billing” webinar

Dear They Said What Nation,

Besides the minor points that your employees’ or dependents’ odds of getting one of these surprise bills are 10 times the odds of having a heart attack or diabetes hospitalization* and that unlike the latter, these bills are utterly avoidable, here are three major reasons to sign up for this webinar:

- The 1500th registrant receives a $100 Amazon gift card from the Validation Institute, assuming they attend.

- You do NOT have to “attend” the webinar to experience it. Registrants will be given the recording. But you do have to register here.

- The way to be certain this is a valuable webinar that will result in easy, major, immediate, behavior change for any employer that implements our elegant solution is that no Koop Award-winning wellness vendor has registered for it — despite the fact that Whole Foods would redeem the gift card for almost all the broccoli you can eat.

A handful of other wellness vendors have signed up. We salute them.

- Aduro

- Health Advocate

- It Starts with Me

- Maestro Health

- US Preventive Medicine

And a special Honorable Mention to Wellable for posting the Reader’s Digest version of the webinar right here.

PS If you are a wellness vendor specifically, and I missed you while scanning the ridiculously long list of attendees, ping me and I’ll add you. Or sign up now and I’ll add you.

*OK, here is the calculation. The lower bound of these odds on any ER visit or admission is about 1-in-5 for any in-network facility according to the Kaiser Family Foundation. Others pace the odds at twice that, but we’ll go with the more conservative estimate. Your covered population incurs about 240 ER visits and admissions in total. 20% of 240 is: 48 per 1000. Whereas the number of covered people who will get a heart attack or have a diabetes event is 2 per 1000.

Oh, did I say surprise bills were ten times as likely? That would make them 24 times as likely.

And yet, unlike heart attacks and diabetes, totally avoidable…

Share this:

Care to guess the odds of a surprise medical bill for an ER visit?

According to a study published in JAMA Internal Medicine, an employee’s odds of getting a surprise medical bill for an ER visit or a hospital stay exceed 40%!

Well, you might say, serves ’em right for not staying in-network.

Wrong. This study looked only at in-network visits and admissions. Thing is, in-network facilities are often staffed with out-of-network providers. I know this firsthand — I’m in a private equity fund that’s making a killing by rolling up provider practices in local markets and keeping them out of network. It’s illegal for provider practices to collude to stay out of network, but it is perfectly legal for them to merge and make a practice-wide decision to stay out of network.

So, wellness vendors and consultants, here are two opportunities you can’t refuse, that are both central to your business strategy:

- Actually do something useful for employees, as opposed to your usual scripted diatribes. Newsflash: employees already know they need to quit smoking and eat broccoli. But they don’t know how to avoid these bills.

- Prevent me from making money.

Also, this is the one thing that could bankrupt them that is totally avoidable. And yet your financial wellness program doesn’t cover it.

Fortunately, if you can spare one short hour on October 31 (which you will get back 38 hours later, when the time changes), you can learn how your employees can avoid these bills. All it takes is a little sticker to put on an insurance card and teaching employees to use their card, rather than sign whatever is put in front of them and/or say: “Same as last year” when they ask you if your insurance information has changed.

The all-star cast of this webinar includes David Contorno, Brian Klepper, Marty Makary, and Marilyn Bartlett. You can register here.

PS If you can’t make the time because of open enrollment, you’ll have access to the recording.

Share this:

A “cure” for surprise medical billing? Webinar featuring Dr. Marty Makary

Attention, employers with wellness programs: this is bigger than broccoli.

No employee bankruptcy has ever been attributed to a broccoli deficiency. By contrast, surprise medical bills like this one are the #1 source of bankruptcies, wage garnishments and lawsuits against employees. You may have a stress management vendor and a financial wellness vendor, But their programs don’t cover the #1 source of avoidable stress related to financial wellness, for the simple reason that they don’t know how.

The Validation Institute to the rescue.

The Validation Institute is doing a webinar describing an actual cure for employee surprise medical bills for emergency visits and admits. it features the leading experts in pricing and surprise billing, including the bestselling author of The Price We Pay, Dr. Marty Makary. Here is the invitation.

October 31st webinar featuring bestselling author Dr. Marty Makary: A “cure” for employees’ surprise medical bills

You think Halloween is scary? Try surprise medical bills. That’s the subject of this groundbreaking October 31st webinar (register here).

Surprise bills may or may not be the #1 source of workplace stress – but they are certainly the #1 avoidable source of workplace stress. 57% of Americans report receiving one on the last five years. If you have not received complaints from employees about them, or noticed wages being garnished by providers, that’s probably because your health benefit is so generous that you are paying these bills without realizing it…inflating your own costs unnecessarily.

And yet there is a “cure,” at least for surprise bills related to emergency visits and admissions. The Validation Institute and Health Rosetta have assembled what they call the “dream team” of experts in pricing and consent-to-treatment to show you – in a mere hour – how to put the kibosh on this scourge. Presenters include:

- New York Times-bestselling author Dr. Marty Makary, whose blockbuster healthcare exposé, The Price We Pay, has already changed some outrageous hospital billing practices, will describe what consent-to-treatment entails, and why your employees should never just sign the forms thrust in front of them

- Industry pricing gurus Marilyn Bartlett (who saved Montana tens of millions through payment reform) and Health Rosetta-accredited broker-of-the-year Dave Contorno will provide a quick lesson in how to avoid paying inflated charges generally

- Quizzify CEO and trade-bestselling author Al Lewis will then combine these experts’ insights into an elegant one-sentence sticker to add to an insurance card that caps charges and avoids overtreatment…while ensuring employees get the care they need.

Attendees will be able to begin solving the surprise medical bills problem within weeks or even days. If you combine Quizzify’s quizzes with the solution as described in the webinar, it will do to surprise medical bills for emergency care what garlic does to vampires.

Here’s the link to the October 31 webinar registration.

Share this:

Surprise medical bill of the week: $650,000 for a $7000 operation

It’s not about the broccoli, folks.

The major hazard facing employees today is not a broccoli deficiency, but rather: surprise medical bills. And here is one that boggles the mind: $650,000 for a $7000 surgery. Even when these emergencies are “covered” (meaning you pay their bill, except for the four-figure co-insurance), these bills create stress, both emotional and financial, far in excess of stress created by any problem that can be solved by eating more fruits and vegetables. The rate of these bills is also about 100 times the rate of diabetes admissions and heart attacks combined: more than half of Americans report receiving one in the last five years.

Further, people — even people who eat plenty of fruits and vegetables — live in fear of receiving one. Often one such bill can force a family into bankruptcy.

So perhaps it’s time to rejigger your wellness priorities in favor of this most pressing problem? And the other thing is, unlike risk factors (which rarely decline in a population by more than 1-2%, excluding dropouts anyway, according to the Health Enhancement Research Organization), this problem is solvable. Naturally, your wellness vendor has no clue how to solve it, so pay close attention to the following paragraph.

The “long version” of the solution can be found here, But if you don’t feel like clicking through to it, here is the short version: give your employees a sticker to put on their insurance card that says:

“I consent to appropriate treatment and to be responsible for reasonable charges not covered by insurance, up to 2 times the Medicare rate.”

Then you need to educate your employees — using Quizzify or an endless stream of memos, as you prefer — to do two things:

- Carry the insurance card and show the insurance card. It’s not enough to say: “Oh, yeah, I’m covered by so-and-so,” and have the intake person verify eligibility.”

- Do not sign the “terms and conditions” they thrust at you. That boldfaced sentence above contains the consent language needed. They have to treat you, based on that consent.

Unlike attempting to create a more broccoli-centric workplace, this is exactly the type of behavior change you can get widespread acceptance of. Nothing like the threat of bankruptcy to motivate employees to put a sticker on their insurance card.