We interrupt our litany of descriptions of failed HRAs to bring you a description of the failure of HRAs.

In wellness, it’s not news to find that something is useless. Indeed, most employees and most economists would agree that the world would not miss Wellsteps or Interactive Health were they to disappear altogether from the earth.

Still, it is news to find that yet another pillar of wellness has fallen victim to actual analysis. In this case, it’s the venerable Health Risk Assessment. This tool has, for about 40 years, been used to encourage employees to pretend they don’t drink. The tool does have one practical use: identifying employees who don’t buckle their seat belts helps employers decide who needs their hearing tested.

HRAs do have their defenders, of whom the most prominent is Larry Chapman, who says they should be treated like “a beloved pet.”

He cites this data set from JOEM showing the costs of people who took the HRA vs. people who didn’t…

…to support the proposition that HRAs cut the average health care cost in half after three years. Or, to use his exact words, CUT THE AVERAGE HEALTH CARE COST IN HALF AFTER THREE YEARS.

It may come as a surprise to Mr. Chapman, who once claimed that wellness could reduce costs by 327%, that CAPITAL LETTERS don’t stand a chance against actual data, and there is nothing whatsoever in this data set that he himself cites to support the notion that HRAs reduce cost by HALF, or for that matter any amount. Indeed, in 5 of the 6 periods studied, the study group had higher costs than the comparison group. The study group did better in the final year, three years after taking the HRA. This is likely because by that time they had forgotten all the useless and, as we’ve been learning, incorrect advice that HRAs provide.

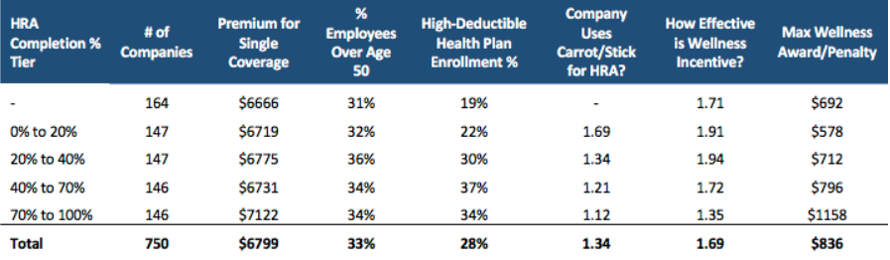

Enter Joe Andelin, who plowed through 200 pages of Kaiser Family Foundation survey data, publishing the results on the American Journal of Managed Care blog on May 1. Lest anyone not be looking forward to slogging through an academic article, let me assure you he sounds more like me than I do, starting with his opening line:

Will Rogers once said, “The income tax has made more liars out of the American people than golf has.” Health risk assessments (HRAs)…could give taxes a run for their money.

The key findings in his transparent and replicable study:

- Incentives and penalties are effective in getting employees to complete HRAs, but…

- …Companies with a high percentage of HRA completion spend more money on healthcare than companies with a low completion rate — and the companies that don’t offer HRAs at all have the lowest spend of all.

I wouldn’t infer causation from this correlation. That’s because most employees, having been burned in the past by (for example) taking HRA advice to get more prostate exams and eat less fat, now have the good sense not to take the advice offered on HRAs like Cerner’s or Optum’s. Rather, I suspect the causation works as follows: companies that actually think completing Cerner’s or Optum’s HRA is a good idea have applied their very stable genius insights to the rest of their health benefit structure…and hence spend more money.

There are plenty of other shocking factoids in this article as well, so I would encourage people to read the link.

You continue to outdo yourself. Excellent.

LikeLike

Find Joe Andelin and thank him

LikeLike

Here is my interpretation of the grid. (1) More companies in the survey do not offer HRAs than do. (2) The premium data column, while interesting, is essentially useless because each company has its own coverage benefits (beyond those mandated by the ACA) which makes a price comparison useless unless you also compare the coverage benefits. What’s covered drives the premium price (3) As for the effectiveness column, effective at what? I could not find a description of the effectiveness being measured here. (4) The higher the incentive or penalty, the higher the completion rate. Obviously this makes sense.

But here is the real question we should be asking: How many employers actually believe that using an HRA alone will reduce their health insurance premium expenses or if self-insured, their actual healthcare spend? Anyone have an answer to this question?

LikeLike

I’ve yet to meet an employer who likes his or her HRA. HRAs are here because they’ve always been here. They’ve outlived any value and are not updated.

LikeLike